FS-2025-0776 | March 2026

The Financial Implications of Housing Needs on the Family Life Cycle

By Troy Anthony Anderson and Michael Elonge

Housing serves as the fundamental physical structure that offers living quarters for both individuals and families. It comprises a variety of dwelling types, ranging from single-family homes to multi-family units, and can be either mobile or stationary. These residences are situated in diverse environments, reflecting a spectrum of living arrangements. Hence, the importance of housing extends beyond mere shelter, fulfilling several critical needs for individuals and families such as, but not limited to:

- Facilitating Daily Living: Housing provides essential space for the daily activities that constitute living, forming the backdrop for routine life.

- Acting as a Familial Hub: It functions as the central headquarters for the family unit, fostering connection and cohesion among its members.

- Ensuring Safety and Security: Housing offers a safe haven, protecting residents from external threats and environmental factors.

- Offering Privacy and Personal Growth: Within its walls, individuals and families find privacy, the freedom for creativity, and an opportunity to cultivate a sense of place and self-identity.

- Fostering Community Connection: A home cultivates a sense of relatedness and belonging to broader societal systems, enhancing social integration.

Consequently, housing is not merely a physical entity but a pivotal component that significantly influences the well-being and social dynamics of individuals and families across the life cycle. As families progress through various stages of the family life cycle- from childbearing and child-rearing to child launching, the empty nest phase, and ultimately, retirement - their housing needs evolve significantly. These stages are not strictly mapped out; rather, they frequently overlap, contingent upon specific family circumstances. The relationship between the spacing of children and the economic status of families is profound, as it directly influences housing requirements throughout the family life cycle. Zulfa, Hasanah, & Kusaini (2024) argue that, when children are born in close succession, particularly in the early years of marriage, families often face financial challenges. This is due to the increased demand for additional living space, food, and other essential resources.

Understanding the dynamic nature of the family life cycle stages underscores the necessity for adaptable housing solutions. As families transition through each phase, they may require new residences or modifications to existing homes to accommodate their changing needs. For instance, the child-rearing stage may necessitate homes with multiple bedrooms and communal spaces, while the empty nest stage might lead to a preference for downsizing or repurposing existing spaces.

Lifestyle choices also play a crucial role in determining the type of housing a family may seek. Families who engage in frequent social gatherings may prioritize a spacious dining room and an expansive patio. Conversely, families with numerous children often prioritize adequate sleeping arrangements and shared family spaces. The dwelling in which a person resides is a significant aspect of their life, reflecting both their current needs and aspirations. Therefore, when contemplating the purchase of a home, it is essential to select a type of housing structure and style that aligns with the evolving requirements of the family life cycle. Such thoughtful consideration ensures that the type of housing structure remains a supportive and nurturing environment, adaptable to the family’s shifting needs over time.

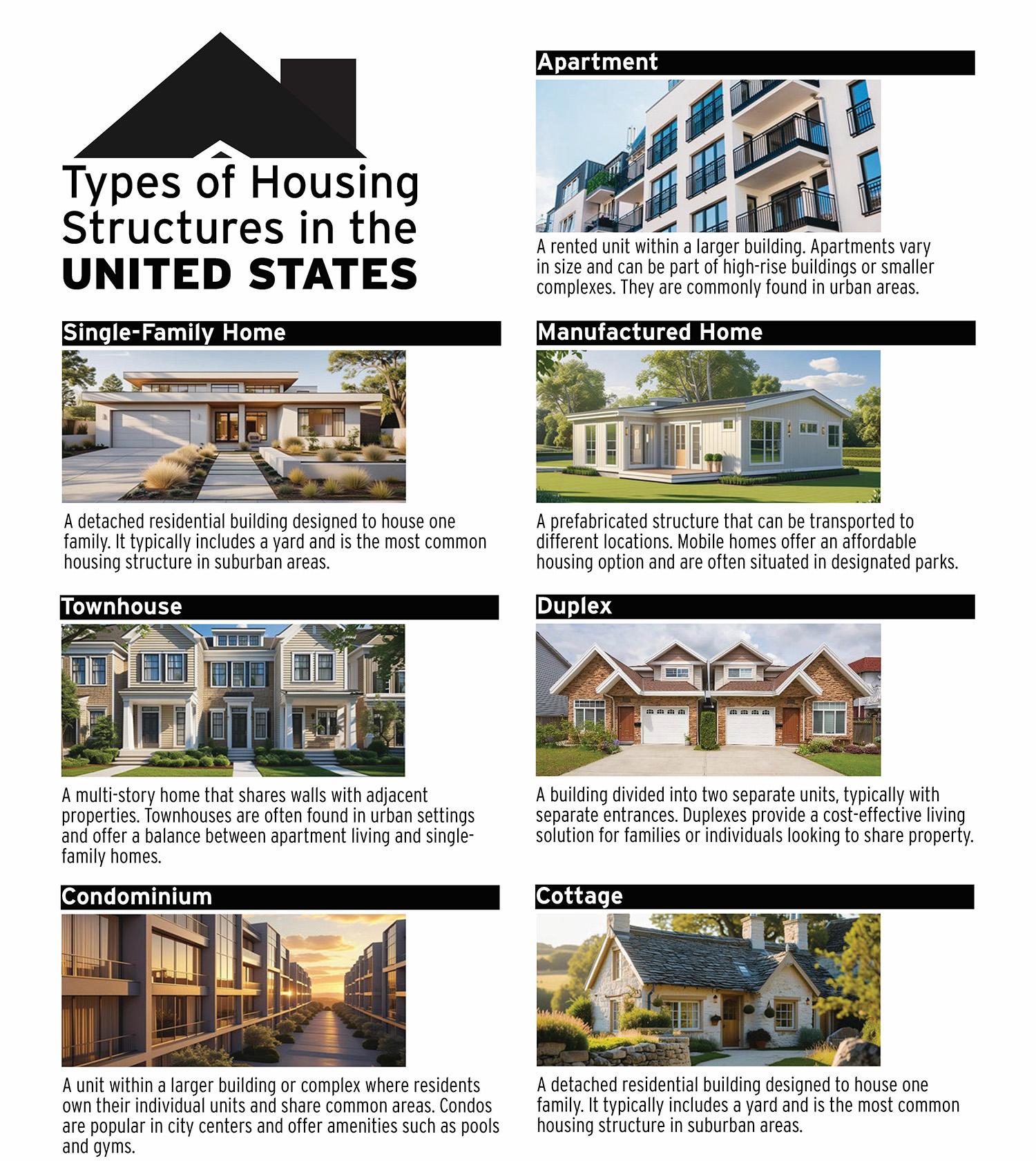

Types of Housing Structures

Whether a person prefers the privacy of a single family home or the convenience of an urban apartment, the United States offers a diverse range of housing options to meet various needs. The infographic below features various types of housing structures commonly found in the U.S. Each type is accompanied by a brief explanation to provide insight into its characteristics and typical usage.

Each type of housing structure offers unique benefits and is suited to different lifestyles and preferences. According to Friedline et al. (2021), in today’s economy, housing is a significant component of a family’s budget and can have profound implications on one’s financial well-being. Therefore, many observers see the overall expense of housing as a widespread problem in the U.S.; whether it’s a modest apartment or a luxurious home, the price can easily burn through years of accumulated savings.

While the diversity of housing options caters to different preferences and budgets, the overarching concern remains the ever-increasing cost of housing, which necessitates a deeper understanding of the financial dynamics at play.

As housing costs continue to rise, it is crucial to examine the various financial factors that impact the families’ ability to secure stable and affordable housing. While it’s vital to determine if it’s a seller’s market - one characterized by high demand and low housing inventory - it’s just as critical to assess if it’s a buyer’s market, with abundant choices and potential price advantages. For many families, soaring housing costs are increasingly hindering homeownership, making it one of the most pressing issues today. The weight of these costs is acutely felt by many individuals and families in pursuit of the so-called “American Dream.” Kim & Renaud (2009) demonstrate that over the past few decades, the price of homes and rental properties have risen out of proportion compared to wage growth as influenced by merit pay, cost of living adjustments (COLAs), bonuses, and/or commissions. This disparity creates a situation in which many families struggle to afford adequate housing without compromising other necessities.

Homeownership – Is it Just a Dream Deferred?

Homeownership remains a cornerstone of the American Dream, symbolizing stability, success, and a sense of community. However, for many families, this dream is becoming increasingly difficult to achieve due to a seemingly endless series of challenges. From financial hurdles to social and economic pressures, the path to owning a home is met with many obstacles that demand careful navigation. This section explores the various challenges that prospective homeowners face, shedding light on the complexities of balancing immediate needs with long-term aspirations. Understanding these challenges is crucial for individuals and policymakers alike, as they work towards creating more equitable and accessible housing within their constituency.

- Expense: For many families, the dream of homeownership is burdened with significant financial challenges, primarily due to the rising and varied expenses associated with family life. As a result, physiological expenses often take precedence over saving for a home, as they are immediate and essential for the well-being of family members.

- Down Payment Requirements: The need for a large down payment, often 20% or more of the home’s price, is a major hurdle for many firsttime homebuyers. With home prices rising, saving enough for a down payment becomes increasingly challenging.

- Mortgage Interest Rates: Any changes, no matter how small, in interest rates can greatly affect the long-term financial burden of a mortgage. Families must carefully consider the implications of financing their homes.

- Property Taxes, Insurance, and Maintenance: Homeownership comes with additional costs, such as property taxes and insurance and maintenance expenses, which can strain a family’s budget.

- Rental Market Pressures: Many rental markets are experiencing rapid rent increases, making it difficult for families to maintain stable housing without spending a disproportionate amount of their income on rent while trying to save to purchase a home.

- Limited Availability: In some areas, there is a shortage of affordable rental units, leading to increased competition and higher prices, which can push families into less desirable or unsafe living conditions.

- Inflation: The pressure of inflation on goods and services means families are increasingly hardpressed to find enough money for housing. As the cost of living, especially housing, continues to outpace wage earnings, individuals find themselves with less disposable income for necessities like food and healthcare.

- Income Inequality: Income inequality amplifies the housing affordability issue. While high income households can absorb rising costs, lower income families struggle to keep up, often leading to a cycle of poverty and unstable housing.

- Government Policies and Support: Government policies play a crucial role in shaping housing affordability. Programs aimed at providing affordable housing or assisting families with housing costs can alleviate some financial pressures. However, the effectiveness of these policies is often limited by funding and implementation challenges.

- Inadequate Amenities and Services: The absence or insufficiency of services such as healthcare, schools, public transportation, or grocery stores present formidable challenges to potential homeowners, particularly for those with young children or elderly family members and can dampen the appeal of owning a home in a particular area.

The journey to homeownership is a challenging one, encumbered by financial constraints, market pressures, and inadequate infrastructure. These barriers not only test the resolve of potential homeowners but also highlight systemic issues that require comprehensive solutions. Addressing these challenges necessitates a collaborative effort among individuals, communities, and policymakers to foster an environment where homeownership is attainable for all. By addressing these challenges, there is potential to help keep the dream of homeownership attainable for future generations, which may contribute to a more cohesive society and support economic stability.

Strategies for Families to Meet Evolving Housing Needs

Despite these challenges, families can adopt a variety of strategies to mitigate the financial impact of housing needs. These include, but are not limited to:

- Budgeting and Financial Planning: Careful budgeting and financial planning can help families manage their housing expenses more effectively.

- Exploring Assistance Programs: Families should explore available government assistance programs, such as housing vouchers, USDA rural eligibility programs, FHA loan, or low-income housing tax credits, to alleviate some financial burdens.

- Considering Location and Type of Housing: Being flexible with location and housing type can lead to more affordable options. Sometimes, moving to a less expensive area or considering alternative housing solutions like co-housing can be beneficial. Co-housing, in this context, describes a shared living situation where people or families inhabit the same residence but keep their own private living areas.

Additionally, some detailed considerations to keep in mind when choosing a home are:

- Site and School District Boundaries: When selecting a home, one of the key factors that families should examine is the relationship between housing, school sites, and existing or proposed school district boundaries. These boundaries can significantly influence the quality of education that children will receive, as school districts typically vary in resources, academic performance, and extracurricular opportunities. Families often aim to reside in areas with highly rated schools to ensure that their children have access to superior educational facilities and a nurturing learning environment. Moreover, the reputation of a school district can have a substantial impact on property values, making homes within desirable districts more sought after and potentially more expensive, yet a worthwhile investment for the long-term benefits. Additionally, understanding site boundaries is crucial, as these determine the specific schools that children will attend, which can affect commute times and the logistics of daily routines. Therefore, when evaluating potential homes, it is essential to research and consider the implications of site and school district boundaries to align with educational goals and family lifestyle preferences.

- Neighborhood: The neighborhood is a critical factor that can significantly impact daily living and future satisfaction. A neighborhood’s character is shaped by various elements, including the community’s culture, safety levels, amenities, and proximity to essential services. A safe and welcoming community can provide peace of mind and foster a sense of belonging. Additionally, the presence of parks, recreational facilities, and community centers can enhance quality of life by offering spaces for socializing and leisure activities. Proximity to schools, workplaces, healthcare facilities, and public transportation can also influence convenience and reduce daily commute times. Moreover, understanding the neighborhood’s future development plans can offer insights into potential property value changes. By considering these factors, prospective homeowners can ensure that their chosen neighborhood aligns with their lifestyle needs and long-term goals, creating a harmonious and fulfilling living environment.

- Aspect: One crucial factor to consider is the orientation of the property in relation to the sun’s path. This consideration can significantly impact the comfort, energy efficiency, and overall ambiance of the individuals living space. A home with a favorable aspect can maximize natural light, reducing the need for artificial lighting during the day and potentially lowering energy bills. For instance, in the northern hemisphere, a south-facing home tends to receive the most sunlight, warming the house naturally during the colder months. Conversely, it provides ample shade in the summer if designed correctly with elements such as overhangs or strategically placed deciduous trees, which offer shade in the summer and shed leaves in the winter to allow sunlight through. The aspect can also influence the views from the windows and outdoor spaces, the growth of gardens, and the overall microclimate around the home. Thus, when evaluating potential properties, it’s essential to consider how the aspect aligns with the family’s lifestyle preferences and environmental goals, ensuring the purchase of a new home is both comfortable and sustainable.

- Family Size: The size of a person’s family is a crucial factor that should be carefully considered. A home that adequately accommodates all family members can significantly enhance comfort, convenience, and overall well-being. For instance, a larger family may require multiple bedrooms to ensure everyone has their own private space, which can help to reduce stress and foster a peaceful living environment. Additionally, a spacious kitchen and dining area may become essential for larger families to gather and enjoy meals together, creating opportunities for bonding and shared experiences. Consideration should also be given to the number of bathrooms, as more occupants typically need more facilities to avoid congestion and maintain a harmonious household. Furthermore, ample storage solutions are vital for accommodating the belongings of every family member, ensuring the home remains organized and clutter-free. Outdoor space is another important factor; larger families might benefit from gardens or yards where children can play safely, and adults can relax. By carefully considering the size of their family and their future needs, individuals can select a home that comfortably accommodates everyone.

The financial implications of housing needs on families are significant and multifaceted. Rising costs, economic factors, and policy limitations create a challenging landscape for many households. However, with careful planning and the utilization of available resources, families can work towards securing stable and affordable housing in today’s economy. Additionally, as families navigate the challenges of evolving housing needs, strategies such as financial planning, resource utilization, and policy advocacy become crucial in securing stable and affordable homes. These proactive measures not only help families maintain their housing but also build resilience against the economic pressures that can lead to housing instability. However, for many, the transition from struggling to meet housing costs to experiencing homelessness can be abrupt and devastating. As a result, the disparity between housing affordability and income levels is a key factor driving people into homelessness when they can no longer keep up with rising rents or mortgage payments. By bridging the gap with supportive housing strategies, communities can work to prevent homelessness and promote sustainable living environments for all.

Homelessness and Affordable Housing in Maryland

In Maryland, homelessness is a multifaceted issue, often amplified by factors such as addictions, disabilities, and mental health challenges. However, at the heart of the crisis lies the inability to afford rent, which remains the central driver of homelessness. When tenants are unable to meet their rental obligations, property owners may seek to protect their income by evicting them. Consequently, evicted tenants who lack alternative housing options often find themselves seeking refuge in the streets or abandoned buildings (Elonge, 2013). This harsh reality reflects a broader trend; for example, in Montgomery County, homelessness surged from 1,144 in 2024 to 1,510 individuals in 2025 (Lynn, 2025). Similarly, Baltimore saw almost 1,500 people experiencing homelessness, underscoring a critical shortage of affordable housing options for families and individuals.

Recognizing the urgent need for affordable housing, the Maryland State Department of Housing and Community Development (DHCD) plays a pivotal role in the development and promotion of such housing across the state. By providing financial and technical resources, the DHCD aims to prevent tenant evictions and support low-income homeowners in avoiding foreclosure. A significant portion of this support comes from the Maryland Affordable Housing Trust, which channels grant funding to county governments, public housing authorities, and nonprofit housing organizations. According to Kelly Jr. (2009), these funds are instrumental in creating stable and affordable housing solutions, thereby reducing the risk of homelessness for vulnerable populations.

Despite concerted efforts and substantial investments, Maryland still faces significant challenges in meeting the demand for affordable housing. The state explores [AK1.1]various options, including transitional housing, emergency shelters, and rental assistance programs, to provide immediate relief to those experiencing homelessness. However, these efforts have yet to fully address the persistent shortage of affordable housing units, underscoring the complexity of the crisis and the need for innovative, sustainable solutions. As of January 2026, Maryland faces an estimated shortage of 94,000 to 100,000 housing units, with a pronounced deficit in affordable rental options for the lowest-income households. The 2025 Housing Underproduction Report by Up For Growth highlights this ongoing challenge, noting a slight decrease from the 96,000-unit deficit reported in 2023. This decrease, though modest, emphasizes the incremental progress made and the continued urgency of the issue.

To address this crisis, Maryland has dedicated substantial resources, including $110 million for rental housing efforts and an additional $50 million for the renewal of vacant properties within Baltimore. These financial commitments reflect the state’s proactive stance in tackling the housing shortage through both immediate relief measures and long-term investments in housing infrastructure. The association of these efforts with the persistent shortage highlights the multifaceted nature of the housing crisis. The Maryland Affordable Housing Land Trust Act provides a useful framework for understanding the scale of the issue and the necessity for ongoing policy reform. The crisis is not merely a matter of supply and demand but involves complex socio-economic factors that require comprehensive strategies to address effectively.

As Maryland strives to close the gap between supply and demand, it becomes increasingly clear that a multifaceted approach, incorporating policy reform, increased funding, and community engagement, is essential to creating a sustainable future where all families have access to safe and affordable housing.

Housing and Government Regulations

The intricate relationship between housing needs and the family life cycle underscores the vast impact that secure and adaptable living spaces have on the wellbeing of families. Housing is not merely a physical structure but a cornerstone of daily life, influencing everything from personal growth to community engagement. The financial implications of housing are significant, with rising costs and economic pressures posing considerable challenges for families striving to secure stable and affordable homes.

Government regulations and policies play a pivotal role in shaping the housing market for individuals and families. While programs aimed at increasing affordable housing availability are crucial, their effectiveness often hinges on adequate funding and strategic implementation. The challenges faced by states like Maryland, as highlighted by both homelessness and shortages of affordable housing, reflect a broader national struggle to address the housing crisis. As a result, efforts to expand affordable housing options are essential and must be accompanied by comprehensive policy reforms that will address the root causes of housing instability.

To create a sustainable future where all Americans enjoy access to safe and affordable housing, a multifaceted approach is also essential. This involves fostering collaboration between federal, state, and local governments, as well as engaging community stakeholders in meaningful dialogue. By prioritizing innovative solutions, such as incentivizing the development of diverse housing types and enhancing support for families through targeted financial assistance, it is possible to address the gap between housing demand and supply.

In conclusion, the path forward requires a concerted effort to balance economic realities with the human need for secure housing. As families transition through various stages of the family life cycle, it is important to support policies that enhance housing stability and affordability. This approach helps provide every family, regardless of their circumstances, with the opportunity to thrive in a home that meets their needs and aspirations.

References

Elonge, M. (2013). Tenant Eviction Prevention: The Impact of Adult Education Intervention in Community Housing. International Journal of Technology and Inclusive Education, Vol. 2, 151-156.

Friedline, T., Chen, Z., & Morrow, S. P. (2021). Families’ financial stress & well-being: The importance of the economy and economic environments. Journal of Family and Economic Issues, 42, 34-51.

Kelly Jr, J. (2009). Maryland’s Affordable Housing Land Trust Act. J. Affordable Hous. & Cmty. Dev. L., 19, 345.

Kim, K., & Renaud, B. (2009). The global house price boom and its unwinding: an analysis and a commentary. Housing Studies, 24(1), 7-24.

Lynn, K. (2025, June 4th). New data reveal progress, challenges in the effort to reduce homelessness in DC region. ABC 7 News. https://rb.gy/iwyrky

Zulfa, V., Hasanah, U., & Kusaini, F. (2024). The phenomenon of early marriage and its impact on family resilience. Journal of Family Sciences, 48-58.

TROY ANTHONY ANDERSON, ED.D

tanders4@umd.edu

MICHAEL ELONGE

This publication, The Financial Implications of Housing Needs on the Family Life Cycle (FS-2025-0776), is a part of a collection produced by the University of Maryland Extension within the College of Agriculture and Natural Resources.

The information presented has met UME peer-review standards, including internal and external technical review. For help accessing this or any UME publication contact: itaccessibility@umd.edu

For more information on this and other topics, visit the University of Maryland Extension website at extension.umd.edu

University programs, activities, and facilities are available to all without regard to race, color, sex, gender identity or expression, sexual orientation, marital status, age, national origin, political affiliation, physical or mental disability, religion, protected veteran status, genetic information, personal appearance, or any other legally protected class.

When citing this publication, please use the suggested format:

Anderson, T., & Elonge, M. (2026). The Financial Implications of Housing Needs on the Family Life Cycle (FS-2025-0776). University of Maryland Extension. go.umd.edu/FS-2025-0776.